In my initial article, I explained the basic premises behind my approach to investing for reliable retirement income. Hopefully, that article peaked your interest to come back and learn how to generate a reliable income from your retirement nest egg without liquidating your principal assets.

Some readers here will have a lot experience with retirement planning and others will be complete novices to retirement investing. Regardless of your level of experience, I would like to lay out some basic terms and definitions to make sure that everyone understands the basic premises and terminology I use, which will make following my line of reasoning easy and you could be on your way to building your reliable retirement income portfolio in no time.

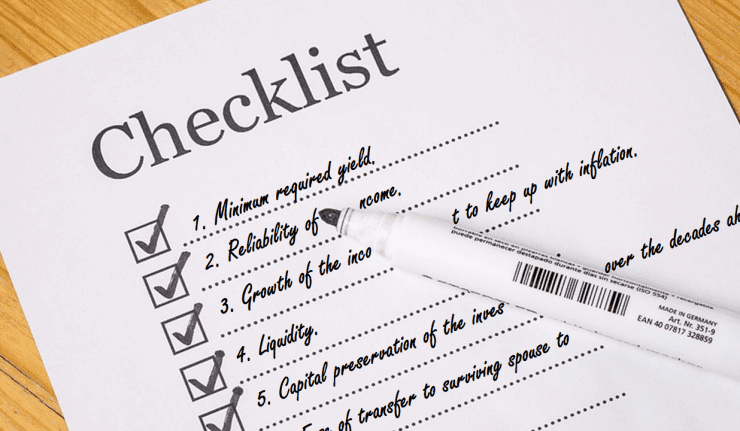

When speaking about income during one’s retirement years, the right place to start is the very beginning: what is it the retiree (which I’ll henceforth use to describe either a single retiree or retired couple) trying to accomplish. This is referred to as one’s investment objective, for which there may be more than one, and each may have its own priority. Each retiree’s investment objective should address the following criteria:

1. Minimum required yield.

Minimum required yield provides the first screening criterion in the search for reliable long term income, and is calculated based on household income requirement and investable assets that are usually a combination of IRA balances, taxable brokerage account balance(s) and other savings that are intended to be used for retirement income. As the required percent of investment – portfolio yield – rises, the income risk rises as well. Once the yield is too high to be practical, the ‘traditional’ retirement planning strategy might require you to liquidate some of your principal by gradually drawing down your investment portfolio over retirement years or by using an insurance product such as a single premium immediate annuity.

2. Reliability of income.

Reliability of income means that the income, like an employment paycheck, will be there regularly, and will have a low risk of fluctuation and a lower risk of being reduced or even eliminated.

3. Growth of the income sufficient to keep up with inflation.

Growth can come from the investments organically growing their dividends over the years ahead, or it may come from the excess income the actual investments produce that are accumulated and used to supplement future household income streams as the inflation rises.

4. Liquidity.

Liquidity is the ease with which investment securities can be converted into cash. This conversion assumes that you can convert your investment funds into cash usually the same day with minimal loss due to trading costs, tax or trade-based market adjustments. This will be a high priority if the retiree feels that a need could arise that would require an unplanned invasion of the principal of the investment portfolio.

5. Capital preservation of the investment principal over the decades ahead.

The conventional assumption is that the retirement savings will be consumed – the savings will decumulate. Capital preservation may be a priority if the retiree will wish to maintain their investment capital to meet future possible household major expenses, such as assisted living or perhaps to establish a testamentary special needs trust – a trust created at one’s death in their estate – to provide for a disabled child or grandchild, to provide for a grandchild’s college fund, to donate a highly valued charitable organization, etc.

6. Ease of transfer to surviving spouse to manage.

In many cases of spousal retirement accounts, only one person is the one who builds, monitor’s and manages the income portfolio. Therefore, it is important to ensure easy transition so that the surviving spouse can continue the management of the income portfolio. If the surviving spouse does not have any interest or necessary knowledge to manage the portfolio, alternative arrangements must be made. This criterion is often overlooked, yet under certain conditions, it may be one of the most important income goals.

With these six basics criteria laid out, we are ready to delve deeper into the detailed steps of setting up your retirement investment for reliable retirement income.

In the next step, I will present a case study based on a couple approaching retirement. I believe that using a specific example will make it easier to explain how the investment objectives outlined in this article might be prioritized, as well as illustrate all the other concepts and actions you need to take to start investing for reliable retirement income.

Bruce Miller is a certified financial planner (CFP) who also is the author of Retirement Investing for INCOME ONLY: How to invest for reliable income in Retirement ONLY from Dividends and IRA Quick Reference Guide.