The three best blue-chip stocks to buy now include a leading electronic payment processing platform, a company known for entertaining millions around the globe and one of the most storied airline manufacturers in the world.

There are two major types of stocks: growth and value. However, many companies like Google (NASDAQ:GOOGL), Tesla (NASDAQ:TSLA) and Microsoft (NASDAQ:MSFT) straddle the line between both categories.

Growth stocks like Lyft (NASDAQ:LYFT) and Square (NYSE:SQ) often see little to no profits and are characterized by high (share) price-to-earnings (P/E) and low earnings-per-share (EPS) ratios. In return, growth stocks often experience rapid revenue gains, resulting in their value boosted by their future earnings and dividends. However, growth stocks generally are viewed as riskier investments.

Blue-chip stocks are large companies with established track records. Blue-chip companies typically fall under value investments. Value stocks are composed of mature companies and household names such as Home Depot (NYSE:HD), Goldman Sachs (NYSE:GS) and Toyota (NYSE:TM). Investors buy value stocks for their current earnings and dividends. Value investments generally possess relatively low P/E and high EPS ratios and are viewed as less risky.

Despite value stocks often being characterized as low risk, low reward investments for individuals seeking safe returns, value stocks have outperformed growth stocks over the long term. Value stocks have returned 1,344,600% since 1926, compared to a 626,600% for growth stocks over the same period.

The case for value stocks has also been tried and tested on Wall Street. Many of the world’s best investors, such as Warren Buffett and Bill Ackman, pride themselves on being “value investors.” Instead of searching for high-risk, high-growth startups that may become the “next big thing,” they seek established companies that have become undervalued.

However, value investing can be tricky. It can be immensely time-consuming to sort through hundreds of well-known companies to discover which value investments are worthwhile and which are not. Luckily, we have done most of the heavy lifting and have identified the three best blue-chip companies to buy now.

3 Best Blue Chip Stocks to Buy Now: #3

The Walt Disney Co. (NYSE:DIS)

The Walt Disney Co. (NYSE:DIS), commonly referred to as Disney, is an international media and entertainment corporation headquartered in Burbank, California. Founded in 1923 by film producer and animator Walt Disney, the company rapidly emerged as a powerhouse in the entertainment industry. Led by aggressive expansion strategies, Disney has since reached a market capitalization (market cap) of $309.1 billion with over a dozen subsidiaries in its portfolio.

According to Abraham Maslow’s famous hierarchy of needs, developed in 1943, there are five physiological needs: food, water, clothing, sleep and shelter. However, at least for the Western world, I would like to propose a possible sixth psychological need: entertainment.

As countries and citizens have grown more affluent and prosperous over the past few centuries, individuals have been able to devote more and more time to entertainment. The average consumer around the world spends more than 7.5 hours per day using media. Americans, meanwhile, consume, on average, over 13.5 hours of daily traditional and digital media.

The universal human-desire for entertainment makes the media industry an excellent investment. After all, Netflix (NASDAQ:NFLX) was the best-performing S&P 500 stock over the last decade, earning investors a 3,726.2% return in the 2010s.

Netflix surpassed The Walt Disney Co. as the largest media company in the world in 2018. However, DIS possesses some significant advantages over NFLX for investors.

The digital video streaming market has seen a massive inflow of competitors in recent years due to Netflix’s success, from HBO Max to AppleTV+ to Amazon Prime Video. To differentiate themselves, streaming platforms have scrambled to create original shows for their viewers. Netflix is expected to spend more than $5.2 billion on original content in 2021 alone.

Despite entering the streaming game late, Disney possesses a sizable lead over its competitors in original content due to its masterful use of acquisitions over the past few decades. With storied companies and studios such as Pixar, ESPN, Marvel Studios, Lucasfilm, ABC and 21st Century Fox in the Walt Disney portfolio, subscribers to Disney+ have exclusive access to numerous fabled franchises, including Star Wars, Hamilton and Marvel Superheroes, to name a few.

Disney+ quickly became the fastest-growing streaming service globally upon its launch in November 2019, surpassing all expectations. Company executives had initially hoped to see 85 million Disney+ users by 2024. Instead, the platform surpassed its goal, and three years early. Disney+ reached 95 million subscribers in March 2021.

Disney also owns Hulu and ESPN+, with 39 million and 12 million subscribers, respectively. The company acquired Hulu as part of its $71.3 billion purchase of 21st Century Fox in 2019. Between Disney+, ESPN+ and Hulu, The Walt Disney Co. is now forecast to become the largest streaming provider in the world, surpassing Netflix, by 2024.

Driven by its streaming services, Disney is projected to experience strong growth for the foreseeable future. Company sales are expected to grow by 12.4% in Q4 2021 and by 25.6% in 2022. As a result, DIS has seen its share price surge by 41.6% over the past year. The upward trend in stock price is displayed below alongside a 50-day moving average.

Chart provided by Stock Rover.

A potential concern for DIS investors is the pricey nature of the stock, compared to its earnings, due to Walt Disney’s new classification as a technology company. Disney currently possesses a (share) price-to-earnings (P/E) ratio of 278.82. However, the company’s immense future revenue and earnings-per-share (EPS) growth mean its forward P/E is forecast at 39.9, well within the industry average of 36.6. Disney has a five-year EPS growth estimate of 47.0%. The Walt Disney Co. has discovered a second wind in the streaming industry.

A discounted cash flow (DCF) analysis, using Stock Rover, values the stock at $207.50, 22.0% higher than its latest closing price of $170.08, earning DIS a “STRONG BUY” recommendation from Stock Rover and a place among our three best blue-chip stocks to buy now.

3 Best Blue Chip Stocks to Buy Now: #2

Boeing Co. (NYSE:BA)

Boeing Co. (NYSE:BA) is an American aerospace and defense company headquartered in Chicago, Illinois. Founded in 1916, 13 years after the Wright brothers first took flight, Boeing is one of the oldest and largest airplane manufacturers globally, with a market cap of $125.4 billion. Today, the company develops and builds airplanes, rockets, missiles, satellites and telecommunications equipment for civilian and government entities worldwide.

Boeing has undoubtedly experienced a rough two years, starting with the grounding of its Boeing 737 Max commercial airliner and ending with the COVID-19 pandemic disrupting the global travel and tourism industry. The company’s stock has more than halved since early March 2019, when it reached $440.00 per share. BA currently trades around $215.00. However, Boeing remains one of the best blue-chip investments available in the stock market.

Boeing’s first sign of trouble occurred in October 2018 when a 737 Max crashed shortly after taking off from Soekarno–Hatta International Airport in Jakarta, resulting in the death of all crew members and passengers. Following a second fatal 737 Max crash in Ethiopia in March 2019, aviation agencies around the globe moved to ground the plane.

The Boeing 737 has become the most successful airliner in history since its introduction in the 1960s. At the time of the groundings, Boeing had an order backlog for more than 4,600 737 Max aircraft and had expected the plane to account for more than a third of the company’s revenue for the next five years. The plane’s tragic accidents and prolonged grounding resulted in Boeing CEO Dennis Muilenburg resigning in December 2019.

The second blow for Boeing came in early 2020 when the COVID-19 pandemic shut down the global travel industry. Airlines quickly began canceling orders for planes after traveler counts and company revenue nose-dived. Boeing experienced 843 airplane order cancellations from January to June 2020.

Although “rough” is a mild way to put Boeing’s challenges over the past two years, it has begun to rebound. The first bit of good news came when the company raised $25 billion in funding in a debt offering in April 2020. The company had initially hoped to raise between $10 to $15 billion but increased the offering due to strong investor demand, following the Federal Reserve slashing interest rates and pledging to dedicate $2 trillion to lending commitments. The offering allowed Boeing to avoid seeking a government bailout.

In addition, the company has essentially emptied its “whitetail” stock. Whitetails are aircraft with no designated buyer. Whitetails are usually rare since most planes are custom ordered. However, due to the 737 Max groundings and COVID-19 pandemic, Boeing was left with 450 whitetail aircraft worth approximately $16 billion in late 2020. As part of its rebound, Boeing, in mid-2021, announced it had less than 10 whitetails in stock, a huge win for the company.

In a final piece of good news, after extensive upgrades and repairs to all outstanding Boeing 737 Maxs, the planes have resumed flights in much of the world, including the United States, India, the European Union (EU), Canada and Australia, among other countries and regions. In a sign of its most popular aircraft returning to form, Boeing announced that it is planning to drastically increase its 737 Max production from its current 19 aircraft per month to 31 in early 2022.

It is important to understand that as one of only two major airplane manufacturers in the world and a North Atlantic Treaty Organization (NATO) defense contractor, Boeing has the backing of the United States government. The United States even fought a 17-year, multi-billion dollar trade dispute with one of its closest allies, the EU, against Airbus for Boeing. The trade dispute officially ended in June 2021 and Boeing looks to be an incredibly safe long-term bet for investors.

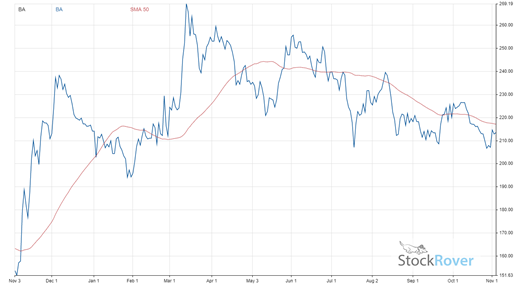

BA already has seen its share price rebound by 43.6% over the past 12 months. With the company forecasted to increase its revenue by 30.6% in Q4 2021 and 35.6% in 2022, BA will only increase further in value. Boeing’s stock price over the past year is graphed below, along with a 50-day moving average.

Chart provided by Stock Rover.

It is not just Boeing that is seeing a rebound. The entire travel and tourism industry is experiencing a faster than expected recovery, bringing further good news for the company. The global travel and tourism industry is expected to recover fully by 2023. The industry is projected to reach $949.6 billion by 2026, fueled by a compound annual growth rate (CAGR) of 17.13% from 2021, as McKinsey & Co. remarked that “a travel boom is looming.” BA has undoubtedly suffered the past two years, but all signs point to an inevitable rebound in the near future.

A discounted cash flow (DCF) analysis, using Stock Rover, values the stock at $267.35, 25.3% higher than its latest closing price of $213.38, earning BA a “BUY” recommendation from Stock Rover and a place among our three best blue-chip stocks to buy now.

3 Best Blue Chip Stocks to Buy Now: #1

PayPal Holdings Inc. (NASDAQ:PYPL)

PayPal Holdings Inc. (NASDAQ:PYPL), founded in 1998, is a financial technology (fintech) company headquartered in Palo Alto, California, specializing in electronic payments and money transfers. The company was acquired by eBay (NASDAQ:EBAY) for $1.5 billion shortly after its original initial public offering (IPO) in 2002, before being spun-off and undergoing a new IPO in 2015. PayPal currently has a market cap of $270.7 billion. The company owns many of the top fintech platforms, including Honey, Venmo, Xoom and Braintree, as its subsidiaries.

In recent years, the emergence of Apple Pay and Samsung Pay has solidified digital payments as the future of monetary transactions. There is no longer a need for consumers to carry cash or even credit cards to shop at most stores. Instead, individuals can now tap a smartphone or smartwatch to pay for goods or services or transfer money easily. As of early 2020, only 19% of small businesses do not accept digital payments.

COVID-19 has helped accelerate the already fast-growing digital payment industry. The industry, which is expected to process $6.8 trillion worth of transactions worldwide in 2021, is projected to grow to a total transaction value of $10.7 trillion by 2025, a compound annual growth rate of 12.2%.

PayPal is by far the largest electronic payment processor in the world with a 49.5% market share. Its closest competitor, Stripe, only controls 16.0% of the market. Despite PayPal’s dominance, the company has not stopped growing. In 2020, PayPal processed $936.1 billion in payments, a 31.5% increase from $711.9 billion in 2019. The company is set for another record-breaking year with $311.0 billion in transactions in Q2 2021, a 40.2% year-on-year increase.

PayPal has continued its progressive business model by announcing in October 2020 that it would allow users to invest in various cryptocurrencies directly from their PayPal accounts.

The main issue surrounding cryptocurrency is its liquidity. Since digital currencies are not a traditionally accepted form of payment, it is difficult for crypto investors to buy goods or services with such assets. An individual cannot directly purchase a sandwich from his local delicatessen using Bitcoin. PayPal can change that.

The company has revealed plans to open digital currencies as a payment method for its more than 26 million merchants in the near future. The move would allow the company to serve the more than 100 million crypto investors worldwide by making it significantly easier for individuals to conduct transactions with their crypto investments. As a further sign of its commitment to digital currencies, PayPal has announced a series of investments totaling $154 million in crypto startups.

PayPal’s investments in cryptocurrency come on the front of the upcoming rollout of the company’s “super app.” The app is designed to resemble China’s WeChat. It is expected to include expansive features beyond mobile payments such as instant messaging, enhanced direct deposit, crypto support, budgeting tools and more. WeChat currently has over 1.25 billion active users. According to PayPal CEO Dan Shulman, the app is now “code complete” and expected to roll out in the coming months. A successful rollout of its super app can allow PayPal to skyrocket well past its current 337 million active users.

PayPal boasts a consistent record of outperforming its competitors. Over the last five years, since its IPO, the company has averaged a sales growth rate of 18.0% and achieved a return rate of 457.1% over the same period. The credit services industry averages are 7.5% and 165.7%, respectively. As a result, PYPL has experienced a 22.7% jump in its stock price over the trailing 12 months, shown below alongside a 50-day moving average.

Chart provided by Stock Rover.

Buying PYPL may not be as flashy of an investment as Apple (NASDAQ:AAPL) or Tesla. However, with a near-perfect Stock Rover growth score of 99/100 and a quality score of 95/100, PayPal is an equity investment with significant upside potential and little to no downside risk.

Despite being a blue-chip stock, the company is still experiencing startup-level growth, with its profit surging by 68% in one year, from $2.5 billion in 2019 to $4.2 billion in 2020. Sometimes the most obvious choice is the best one, and investing in PayPal is one of those choices.

A discounted cash flow (DCF) analysis, using Stock Rover, values the stock at $320.76, 39.2% higher than its latest closing price of $230.38, earning PYPL a “STRONG BUY” recommendation from Stock Rover and a place among our three best blue-chip stocks to buy now.

Capison Pang is an editorial intern who writes for www.stockinvestor.com and www.dividendinvestor.com.