Benjamin Franklin famously said, “Nothing can be said to be certain, except death and taxes.” And with those taxes going up dramatically recently, safeguarding your money in legal ways is becoming more important than ever. In the following report, I’ll give you four different legal loopholes you can take advantage of to protect your money from the greedy hands of big government.

Loophole 1: Tax-Deferred Annuities

Three different tax-deferred annuities are worth bringing to your attention. Annuities are insurance products, so I always try to focus on creditworthy insurers that are stable and well managed. To help me assess annuities, I rely on annuity experts David and Todd Phillips, a father and son team that operates Estate Planning Specialists, an Arizona-based division of Phillips Financial Services. For a limited time, Phillips Financial Services will provide a 104-page paperback book on annuities for a nominal price of $4.95 to cover shipping and handling, if you call 1888/892-1102. In the book, you will learn how to crash-proof your portfolio and still benefit from the upside of the stock market.

Annuity #1: As a CD alternative, consider the top fixed-rate annuity, which currently is paying a guaranteed set rate of 3.75% interest for 10 years. A $100,000 deposit will produce an annuity worth $144,504 within 10 years. Thanks to annuities’ inherent tax-deferral, assuming a 28% tax rate, the tax-equivalent yield is 5.21%.

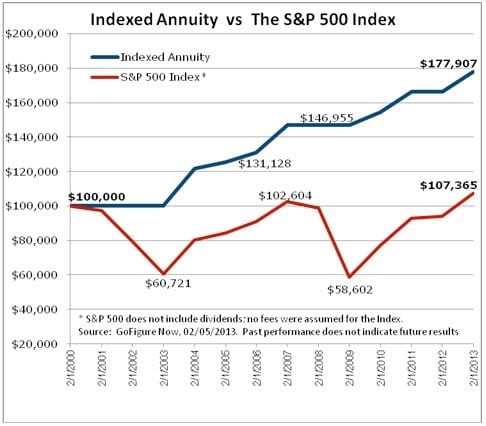

Annuity #2: A second annuity is one favored by my wife, Jo Ann Skousen. Jo Ann’s favorite is an indexed annuity that is designed never to lose money, but only participates in stock market gains, as measured by the S&P 500 Index. This annuity also protects you from stomach-churning market plunges. It offers the best potential return of any annuity of its kind in the country, according to my experts. This annuity produces a return of up to 3.05% per month. If the annuity grew at least that much each month for a full year, you could make up to 36.6% in a single year. The annuity also resets each year and locks in the previous year’s profits.

Annuity #3: The third annuity that I want to highlight for you is one that I call the “Best-Income Annuity.” I call it a Hybrid Longevity Annuity, since it guarantees you an income stream that will last as long as you or your spouse lives. It is hybrid because it includes two features typically separated but included together in this unique investment.

This annuity is similar to the preceding one, since it offers the same potential for long-term growth, but it also provides guaranteed income for life. This annuity is a hybrid of the indexed variety that also offers guaranteed income for life. The hybrid annuity provides income to retirees to help them avoid running out of money.

The traditional solution for guaranteeing lifetime income used to be through lifetime payout annuities also known as Single Premium Immediate Annuities (SPIAs). The drawbacks to the SPIAs are twofold: 1) You lose control of the asset, essentially turning it over to the insurer in exchange for receiving the lifetime of income, and 2) Committing to a SPIA in current market conditions is like signing up for a 30-year, low-yielding bond that you can’t escape. Industry insiders are calling it “committing Annuicide.”

With the Hybrid Indexed Annuity, you get the best of both worlds. You keep the guaranteed lifetime income, but still maintain control of your principal as well as any interest earned from the performance of your chosen stock index. And just like the previous annuity, your principal investment is completely protected from market losses. My experts tell me that in some cases you can actually be guaranteed more income with the top paying Hybrid Indexed Annuities than found in most competitive SPIAs.

If you are married, I recommend including your spouse on the income; that way, it pays as long as either of you are living. Typically, adding a spouse will reduce your lifetime payout between 5-10%.

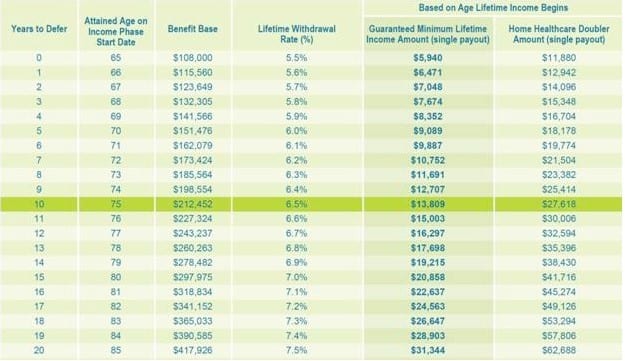

Buyer Beware: Not all income riders are created equal. In my team’s research, I’ve found a huge discrepancy between the different contracts. For example, one of the more popular income riders will pay $9,075 per year for life, assuming a 65-year old deposits $100,000 and waits to start taking his lifetime income until age 75. Digging a little deeper we uncovered a plan that would guarantee that same annuitant $13,809 per year, also starting at 75. That performance results in more than 50% more income per year!

Our experts also have several plans that will increase your income up to 100%, if you become disabled or need long-term care assistance. For example, our 75-year old could double his $13,809 for long-term care and receive $27,608 per year provided he got a doctor’s note stating he could not perform two of the six Activities of Daily Living (ADLs).

Don’t be fooled by huge upfront bonuses or guaranteed roll-up rates. Income roll-up rates can range between 4% and 10%. If you’ve been to a financial advisor’s dinner seminar lately, you may have heard some of these “incredible offers” with eye-popping phrases like “Get 8% guaranteed growth” or “Learn how to get a 45% bonus.” Be sure to read the fine print. First, know the difference between compounding and simple interest. For example, 8% simple return will yield the same as 6.05% compounded over 10 years.

Most importantly, don’t lose sight of the bottom line: Your guaranteed takehome income payment. In our example above, both had the same guaranteed roll-up rate, but the $9,075 annuity only lets you take out 5% per year at age 75, whereas the $13,809 annuity pays out 6.5%.

Loophole 2: 401(k)s and IRAs

There are a number of ways to save for retirement. 401(k)s and Individual Retirement Accounts (IRAs) are two of the most popular. If you’re not quite sure how 401(k)s and IRAs differ, the following information should help.

401(k) Retirement Plans

This is a savings plan set up by employers for their eligible employees. Company management teams decide for themselves what qualifies as an eligible employee. Such employees may elect to contribute a portion of each paycheck to their retirement plan (up to a preset maximum percentage set by the company or the IRS). However, such contributions are not pre-tax: they come out of the employee’s take-home pay. “Qualified” Plans allow earnings accrued within the retirement plan to be eligible for tax deferment benefits.

Employers also may match employee contributions (up to a certain percentage, again set by the company or IRS). In addition, employers also may structure their 401(k) Plans to allow for profit-sharing contributions. Should the Plan allow employees to direct their own investments, the company will provide a core group of investments from which to choose. Or, the company may choose to have investments directed and managed by a professional.

Employees may be allowed to withdraw funds from a 401(k) Plan. These fund distributions are subject to limitations set by the company and the IRS, and they are subject to state and federal taxes. They also may be subject to additional penalties, should withdrawals be made before the employee reaches retirement age as defined by the Plan.

Finally, you should check with your employer for the specifics governing your company’s Plan, should they offer one. For more information, refer to my source for 401(k) information: investopedia.com.

Individual Retirement Accounts (IRAs)

IRAs are savings plans that allow for the investment of funds from within the account as a way to build additional value. There are several types of IRAs, each with their own specific benefits:

- Traditional IRAs

- Roth IRAs

- SIMPLE IRAs: Savings Incentive Match Plan for Employees of Small Employers

- SEP IRAs: Simplified Employee Pension

Traditional and Roth IRAs are created by individual taxpayers (often with the help of a financial advisor). IRA owners are allowed to contribute 100% of their compensation (in the form of self-employment income for sole proprietors and partners). However, each type of account will have a fixed maximum dollar amount that can be contributed. Contributions to the Traditional IRA may be tax deductible depending on the taxpayer’s income, tax filing status and coverage by an employer-sponsored retirement plan. Roth IRA contributions are not tax-deductible.

SIMPLE IRAs are plans established by employers, including self-employed individuals, whereby the employer is eligible for a tax deduction for contributions. Employees may make salary deferral contributions to their SIMPLE IRAs, while employers have two choices when contributing to an employee’s SIMPLE IRA:

- Match the amounts that each employee makes toward his or her own elective-deferral contribution up to 3% of the employee’s annual compensation.

- Make a flat 2% non-elective contribution to all qualified employees, regardless of whether the employee makes any contributions.

SEP IRAs are retirement plans created by an employer or self-employed individuals. Employers can contribute to an employee’s SEP IRA on a discretionary basis and are eligible for a tax deduction when such contributions are made. Contributions to a SEP IRA are immediately vested at 100% and are directed by the IRA owner.

Withdrawals from an IRA (except for Roth IRAs) will be taxed as income, including capital gains. Distributions from a Roth IRA are tax-free. Withdrawals or distributions taken after retirement may be taxed at a lower rate, as income is generally lower after retirement. Also, depending on income, an individual may be able to fit into a lower tax bracket with tax-deductible contributions during his or her working years while still enjoying a low tax bracket during retirement.

For more information, refer to my source on IRAs: investopedia.com.

Loophole 3: REITs

Real Estate Investment Trusts also are known as REITs (pronounced like beets). They offer independent investors an opportunity to bank two-for-one profits from growth in distinct sections of the real estate market.

Investors purchase shares of REITs just like any other equity. As the value of those shares appreciates, they collect the gains. In addition, REITs are required by law to pay out 90% of their profits to investors in the form of dividends. So, when you’re a REIT investor, you’re receiving regular dividend income and capital appreciation… Not too shabby.

Here’s a quick example to illustrate how they work. First, REITs borrow money at, say, 1% and then invest it into a portfolio of real estate-related assets. In this case, we’ll say mortgage-backed securities. It then leverages that investment… or invests a multiple of every dollar it has under management. The returns on these investments create the profits used to pay out dividends.

As you probably realize, as long as REITs can borrow funds at such low rates, they have a better shot at creating profits for investors. So keeping an eye on the interest rate environment is crucial to knowing when to invest in REITs – a message I delivered to readers of Forecasts & Strategies.

So how long can interest rates stay low? In the United States, as of October 2015, three-month T-bill rates were 0.03%, 10-year Treasuries were up to 2.16% and 30-year Treasury rates returned 2.94%. The 30-year mortgage rates were 3.88%. Once price inflation picks up, interest rates will rise sharply, so avoid variable-rate mortgages and highly leveraged mortgage REITs.

With that situation in mind, let’s look at a couple of REITs that we’ve either owned in the past or are active recommendations today:

REIT Play #1: You may be surprised to learn that REITs can offer you an outstanding return on investment, even when the housing market is off. Take our F&S investment in Annaly Capital Management (NLY) from August of 2009 until 2011.

At the time, mortgage-backed securities, like the ones invested in by NLY, had become cheaper as investors avoided real estate and banks purged their balance sheets of assets that they deemed risky. NLY seized the opportunity to borrow at low rates and bought depressed securities. And with real estate showing signs of bottoming at the time, Annaly was in a good position to profit. So we purchased it and ended up with a 28.5% gain when we sold in 2011. Not bad, especially when you considered the housing market continued to stagger almost the entire time.

However, mortgage REITs like Annaly are highly leveraged and seek to profit from the yield curve. When interest rates start rising and the yield spread narrows, mortgage REITs will have to cut their dividend and the price could fall. In fact, more mortgage REITs, including Annaly, have cut their dividend in 2012. That’s why we have sold our position.

REIT Play #2: Inland Real Estate (IRC) was a recommendation in Skousen’s High-Income Alert (SHIA), my trading system that profits from investing in dividend-paying stocks and buying options on them at the same time. When I recommended IRC, here’s what I told readers at the time:

Based in Oak Brook, Illinois, Inland develops, owns and operates retail shopping centers on 150 commercial properties throughout the Midwest and southeast. That’s nearly 15 million square feet of real estate worth approximately $2 billion. This REIT has a young and aggressive management team which has been actively buying its own stock over the last several weeks. It’s a classic buying cluster, a very positive signal. Currently, you can look forward to a 5.5% dividend yield in addition to any capital appreciation.

So, we bought shares along with March 2013 call options. Oh, I should tell you that on Feb. 11 of that year, I told subscribers to pocket a 556% profit from those options!

Here’s a chart of IRC’s activity during the last year:

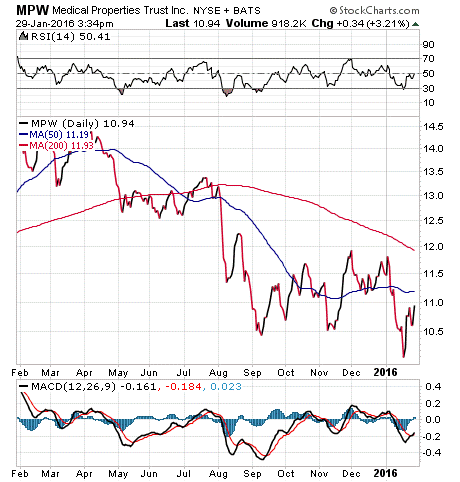

REIT Play #3: Next, I recommended Medical Properties Trust (MPW) to SHIA subscribers on January 8, 2013. Here’s how I presented it to investors at the time:

MPW focuses exclusively on providing capital to acute care facilities through triple-net leases. (That situation means the tenant is responsible for real estate taxes, insurance and maintenance.) By allowing health-care operators to tap the value of their real estate and channel it, MPW enables hospitals to increase their returns from what they know best – operations. The trust has been amazingly successful with this formula. In fact, MPW has grown its assets to more than $1 billion in less than five years. And current numbers look remarkable: Revenue jumped 62% last quarter, operating margins hit 62% and profits are set to jump. Management shares my view, as Director Glen Orr, Jr. bought a substantial number of shares, spending more than $1 million. That’s a strong vote of confidence.

Here’s a chart of MPW’s performance during the last year:

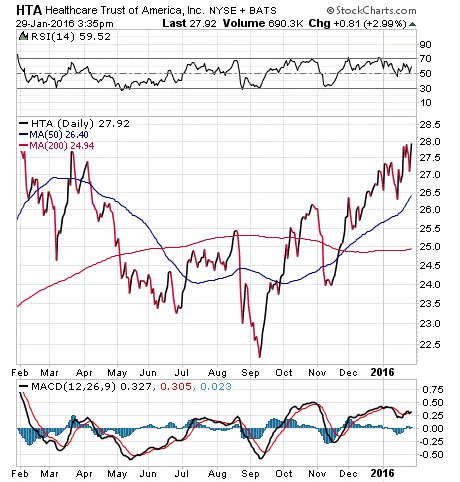

REIT Play #4: The final example is also from SHIA. It was Healthcare Trust of America (HTA), recommended on February 11, 2013. Here’s what I said at that time:

HTA is a real estate investment trust (REIT) headquartered in Scottsdale, Arizona, that invests in medical office buildings and healthcare-related facilities. And healthcare REITs provide us with a steady, recession-resistant business. Unlike many trusts, HTA doesn’t farm out property management responsibilities. HTA is a fully integrated, self-administered, self-managed REIT that oversees its own day-to-day operations. This keeps costs low and net income high.

HTA owns $2.6 billion worth of property totaling 12.5 million square feet, operating in 27 states, including key cities such as Atlanta, Phoenix, Pittsburgh, Boston, Dallas and Houston. Occupancy rate tops 91%. The trust is well managed and has grown organically and through acquisitions, when it could pick up new properties on the cheap.

I also saw good capital gains potential, so I told subscribers to buy shares along with July call options.

Here’s a chart of HTA’s performance over the last year:

Loophole 4: Business Development Companies

Business development companies (BDCs) are ideal to shelter income inside businesses. Businesses and corporations remain the primary tax shelter of today, and taxpayers would be wise to keep much of their assets and income inside a sheltered corporation. They are like REITs, in that they don’t have to pay income taxes if they distribute 90% or more to shareholders. So BDCs tend to pay high yields.

Let’s take a look at two business development companies that I’ve recommended in the past: MAIN, from Forecasts & Strategies, and PSEC, from my former service Hedge Fund Trader Alert.

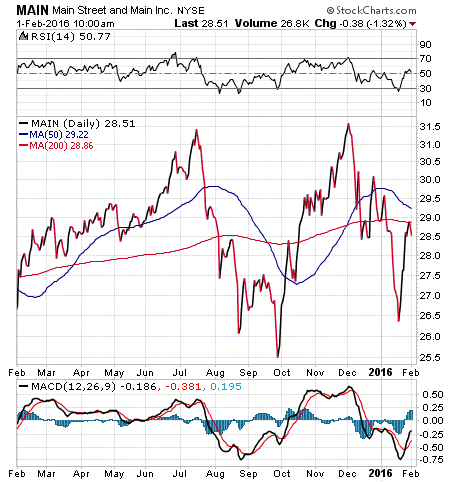

Business Development Company Play #1: Main Street Capital Corp. (MAIN), based in Houston, is a business development company that makes loans and takes equity positions, as well as engages in buyouts, recapitalizations and growth financings to small and mid-sized companies. Typically, these businesses are cash flow positive, with revenue between $10 million and $100 million. Main Street is well diversified, with holdings in the commercial services, energy and media sectors.

One of Main Street’s more appealing qualities is its dividend, which is paid monthly. It has never been cut since the 2008 financial crisis and, in fact, the company raised its dividend six times since 2012. Add to this monthly dividend stream a special bonus dividend paid out in December and June, and you begin to see what a good deal it is to own this company. Like real estate investment trusts (REITs), business development companies like MAIN pass along gains in the form of dividends, thereby avoiding corporate taxes.

Main Street is well positioned to take advantage of new opportunities. It has plenty of cash and marketable securities. And its earnings are top-notch.

Management team members also are accumulating the stock for their own accounts. Main Street’s management team and directors own a huge portion of the company. Now, that’s what I call confidence in the firm. The management team’s interests are clearly aligned with shareholders. If the business does well, and management is able to increase the dividend, they’ll be putting more money directly back into their pockets, the way it should be.

It’s rare to find a stock with a high-yield, growing dividend, a very solid management team, insider buying and bright prospects for the future. But that favorable situation is exactly what Main Street Capital offers.

Here’s a chart of MAIN’s performance during the last year:

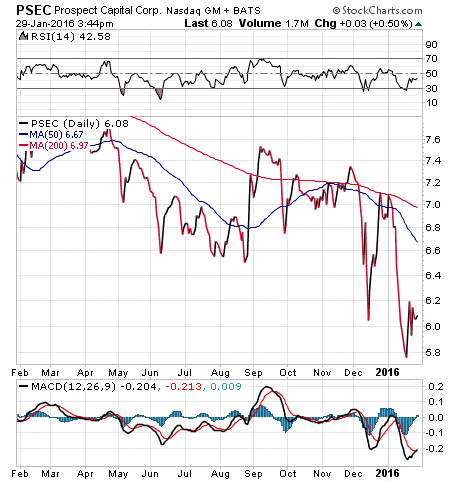

Business Development Company Play #2: Prospect Capital Corp. (Nasdaq: PSEC) is a New York-based business development company. Founded in 1988 and publicly traded since 2004, this closed-end investment company provides capital to more than 60 private and micro-cap public businesses in the United States and Canada, including those engaged in energy, health care, manufacturing and specialty minerals.

The company has paid a dividend since its inception as a public company, especially during the financial crisis of 2008, when it adopted a policy of a high and rising dividend, and its generous monthly dividend has been around since March 2010. All of this results in PSEC’s impressive double-digit percentage yield.

Company insiders are high on Prospect Capital. Not surprisingly, they have started buying again, and PSEC is benefitting from this heavy investment. Notably, Prospect has seen strong insider buying by its Chief Financial Officer (CFO) Brian Oswald. When the CFO buys stock in his company, I pay attention. It’s even a better sign than when the CEO buys. Of course, CEO John Barry has bought PSEC stock. Other officers and directors have bought stock, too.

In other good news for PSEC, venture capital projects are especially hot right now with the fracking technology in South Dakota and Montana. The company also benefits from the Fed’s current low-interest-rate policy. By keeping interest rates low, it pays banks and other financial institutions to play the yield curve, and to buy safe Treasuries and government-backed mortgages with cheap loans from the Fed (0-0.14%), NOT by making risky loans to small business (the engine of job creation). Prospect Capital is firing on all cylinders right now.

As business development companies like Prospect Capital are stepping into the void and offering alternative sources of financing, PSEC is growing fast; revenues and earnings are strong.

As PSEC aggressively expands its portfolio, the company continues to rally from the financial crisis, including several recent quarters with double-digit percentage growth, in the face of these increasing revenues, earnings and dividends.

Here’s a chart of PSEC’s performance during the last year:

I hope you enjoyed learning about the legal loopholes which allow you to keep safe, and even grow, your hard-earned money. Remember, there never was a tax law passed which did not have legal loopholes, and finding those loopholes can be the key to personal prosperity.

Here’s to your continuing success.

![]()

Mark Skousen

Editor, Forecasts & Strategies