After outlining six important retirement estate planning criteria in a previous article, I will use a case study of a soon-to-retire couple to explain how to prioritize these criteria, so that you can focus on the most important aspects first when building your own portfolio for reliable retirement income.

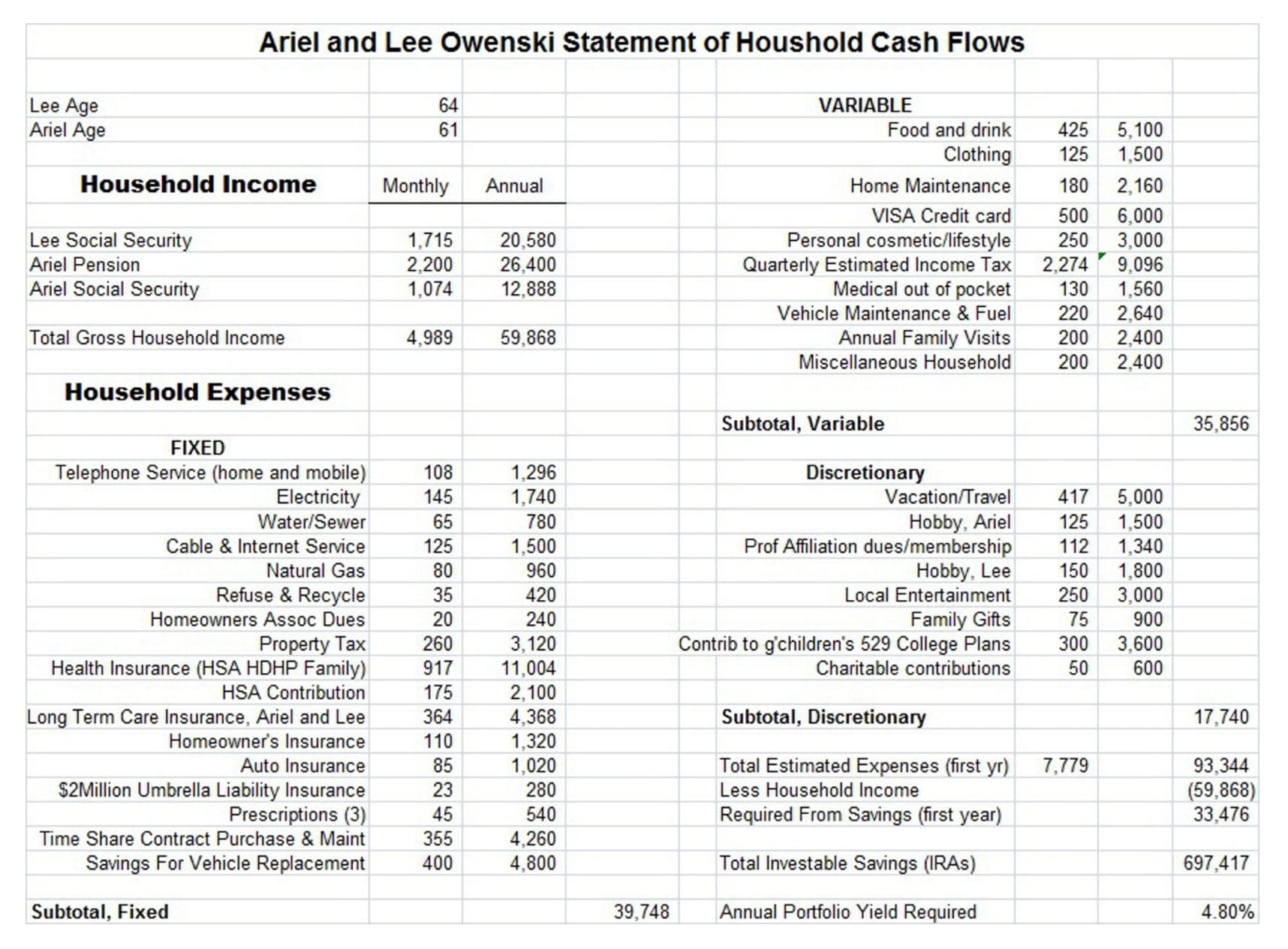

The spouses in our case study couple, Ariel and Lee Owenski, are going to be retiring from their jobs at the end of this year. Ariel has a pension from her non-government employer that will pay a fixed payment of $2,200 per month. Lee does not have a pension. You can see additional details in the table below.

The Owenski’s estimate that their monthly household income need is $7,780, which covers all their planned fixed, variable and discretionary expenses. This includes the typical monthly expenses that you can see on the below household cash flow projection for their first retirement year. They anticipate a 3% living cost every subsequent year, mostly for insurance, food and energy costs.

Ariel and Lee have rolled over their retirement plan savings into their existing Traditional IRAs (TIRAs). With the rollover and past direct TIRA contributions the accounts have about $800,000.

They will begin their Social Security early next year (4 months after formally retiring) when Ariel attains age 62 and Lee is 3 months from age 65. The combined household social security benefit will be $2,789 per month. They have a cash reserve of close to $15,000 to cover any unplanned emergency expenses that may occur and they have set aside $100,000 of their IRA savings in a separately established TIRA invested in an FDIC insured CD with their Credit Union.

Additional monthly income from investments

With a need for a $7,780 income each month – $93,360 per year – and a fixed income of $4,989 – Ariel’s pension of $2,200 and $2,789 from their combined Social Security payments – their investment savings will need to provide $2,871 per month or $33,492 per year, which represents about 4.8% of their retirement savings available for investing.

Ariel and Lee carry identical long-term care insurance contracts with $4,500 monthly maximum benefits for up to 36 months. The current combined premium for both policies is $4,368 per year. While the Owenski’s expect this annual premium to increase in the future, they do not the increase amount.

Other important insurance needs include their health insurance which under the not-yet-repealed Affordable Care Act standards is a high deductible family health plan combined with a tax favored Health Savings Account, with a current balance of about $8,500.

The plan carries an annual maximum out of pocket cost of $6,000 for the family, which they will carry until they attain age 65 and begin Medicare and a Medicare Supplement policy. The monthly cost of the Medicare parts B and D coverage’s and Medigap coverage’s, with lower annual maximum out-of-pocket costs, will cost slightly less than what they currently pay. Finally, they carry a $2 million umbrella casualty policy as a high supplemental coverage for their autos and homeowner’s casualty coverage.

Ariel and Lee have no plans to move while they are still able to live unassisted. Their house has a fair value of $270,000 and the mortgage is fully paid. Unless they must sell the house in a true financial crisis, the Owenski’s hold their house in a revocable trust and plan to leave it to their children at their death or to sell it if they must move into a nursing home or assisted living.

Statement of household cash flows

Below is the Owenski’s Statement of household cash flows.

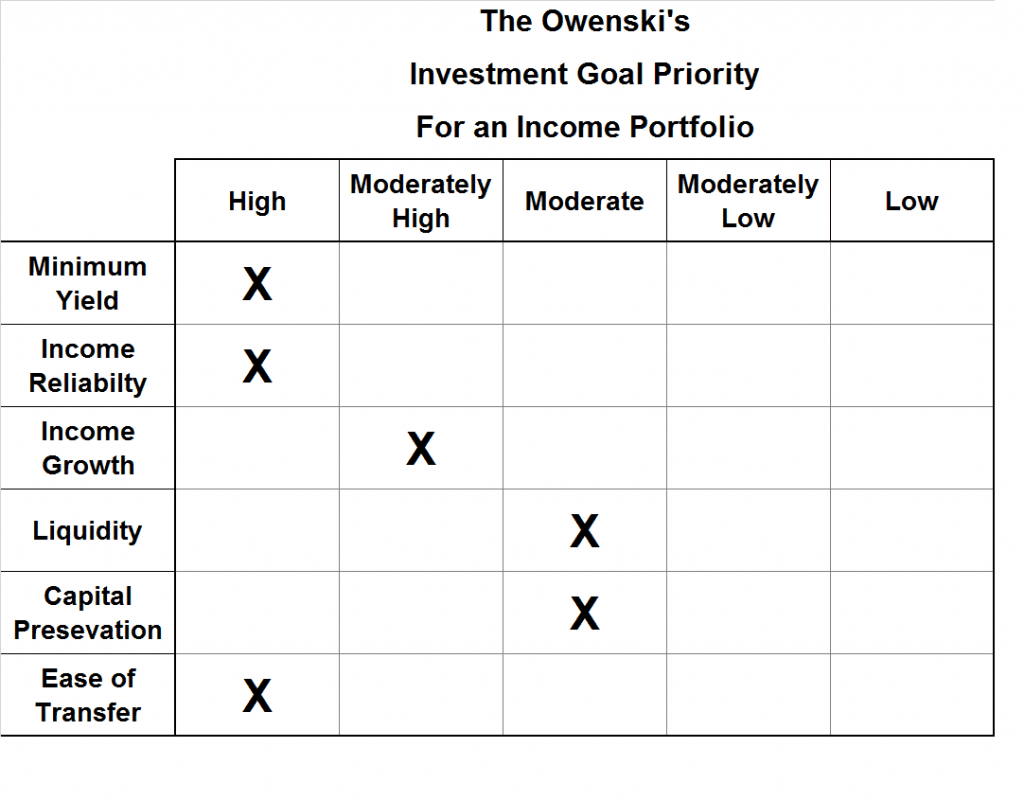

Considering the Owenski’s current situation, what will be their primary income investment objective and which of the six criteria should they prioritize?

Considering the Owenski’s current situation, what will be their primary income investment objective and which of the six criteria should they prioritize?

I will use a prioritization scale of High Priority, Moderately High Priority, Moderate priority, Moderately Low Priority and Low Priority to rate the potential income investment objectives.

Minimum required yield: High priority

It is very important to make that you meet your investment yield target to ensure sufficient funds to supplement any fixed income payments. Ariel and Lee’s current target is a 4.8% of investment portfolio as income each year:

Reliability: High priority

The income inflow must be steady to cover regular monthly expenses.

Growth of Income: Moderately high priority.

Social Security which represents 56% of the Owenski’s household income before IRA withdrawals is already adjusted for inflation each year.

Liquidity: Moderately low priority.

The Owenskis are well covered for potential unexpected large losses to their savings and have an adequate emergency fund and emergency reserves – their home and long term CD – to pay for the unexpected large expenses.

Capital Preservation: Moderate priority.

Although this couple doesn’t foresee any expenses late in life, other than reliable income, they are concerned with the future costs of assisted living and nursing home care beyond what the long-term care insurance would cover. Additionally, they would like, if possible, to leave an inheritance for their 2 children and 7 grandchildren, although this is a moderately low or low priority.

Ease of portfolio management to surviving spouse: High priority.

If Lee dies first, he feels it is important for Ariel or one of his adult children to be able to manage the investments to continue to provide the required household income.

Here is a summary table showing these goal priorities for their income portfolio:

Under these circumstances would a pure income portfolio provide enough income to meet Ariel and Lee’s needs? Would a pure income portfolio meet their investment objectives? To answer these questions, I will first explain in an upcoming article a little more about what an income portfolio is and, perhaps more importantly, what an income portfolio is not.

Bruce Miller is a certified financial planner (CFP) who also is the author of Retirement Investing for INCOME ONLY: How to invest for reliable income in Retirement ONLY from Dividends and IRA Quick Reference Guide.