The stress tests conducted on the 35 largest banks within the Fed’s sphere of influence resulted in what I would call “wishy-washy” actions, considering the latest resurgence of the pandemic and the potential economic implications it presents.

At the forefront of conducting these annual stress tests is the task of determining how bad losses can get and ensure that banks have enough loss-absorbing capital to avoid systemic distress and allow them to lend to businesses and consumers. Second-quarter reporting season is about to get underway and the big banks will be posting their results during the week of July 13.

So far, there has been little transparency as to how many businesses and people have fallen behind on their obligations. This past Thursday, the Fed voted to require large banks to preserve capital by suspending share repurchases and capping dividend payments in the third quarter. In a four-to-one vote, the Fed will tie the distribution of dividends to a formula based on recent income.

The formula sets third-quarter dividends at a level equal to average net income over the past four quarters. Fed Gov. Lael Brainard dissented from the decision. By that calculation, some banks may have to cut their dividends. A senior Fed official said this could be “binding” for some banks. In her dissent, Brainard said, “I do not support giving the green light for large banks to deplete capital.” Instead, she argued for a blanket suspension of dividends.

This week’s stress revealed the limitations of the current regulatory regime and the need to tighten its criteria, and soon. The tests’ original worst-case scenarios, devised in February, before the coronavirus crisis took hold, included shocks such as a 10% unemployment rate, which is woefully behind the current employment situation.

To compensate for a more real-time measure of financial resilience, last week’s stress tests stated that regulators performed a separate “sensitivity analysis” that featured harsher scenarios. In doing so, the regulators erred by not disclosing bank-specific loss estimates, citing the “limitations” and “considerable uncertainty” created by the pandemic. That’s “Fedspeak” for “We don’t want to rattle the markets.”

In today’s regulatory environment, the stress tests rely on regulatory capital measures that are imprecise when the ground has suddenly shifted under the economy, such as unemployment data, and often is at odds with market-based measures that reveal more about a bank’s health. There’s a big difference between the two measuring models.

What’s a “market-based measure?” In avionics, market-based measures are instruments that are designed to address the “climate impact of aviation” beyond what operational and technological measures or sustainable aviation fuels can achieve. It is a set of measures to reflect radical change outside of conventional tools. To say there is a “climate impact of normal banking conditions” from COVID-19 is an understatement.

This latest round of stress tests fell short of laying out the climate impact of internal operations — specifically hard and detailed data on bad loans. Instead, banks have been steadily raising dividends and buying back record amounts of stock right through the first quarter and, in some instances, during the second quarter while jawboning about how well things are going in the midst of record layoffs and shuttered businesses.

The lack of transparency will not “bolster public confidence,” as Fed Vice Chairman for Supervision Randal Quarles expects. On the contrary, it is already undermining trust, leading observers to speculate that potential losses must be severe if they cannot be made public. And while the biggest banks might manage through a second wave of the coronavirus intact, scores of regional and smaller banks run the risk of being undercapitalized in the coming months for not having taken more aggressive measures to preserve capital.

The Fed, in all its good intentions to produce optimism in the credit markets and investors alike, may have underestimated the number of underperforming assets early on in the pandemic, which triggered its aggressive fiscal stimulus actions during the past several weeks. While it is very difficult to predict the scale and scope of something like COVID-19, it may show, in hindsight, about a month from now that the Fed should have restricted all dividends and buybacks back in late March.

According to the Fitch credit rating service: “Before the coronavirus pandemic, the delinquency rate had been steadily falling, and stood at just 1.31 percent in March. Now it’s expected to reach as high as 8.75 percent by the end of September — approaching its peak of 9.01 percent recorded in July 2011.” (Source: www.therealdeal.com)

Fitch’s delinquency projections don’t include loans in forbearance. Many borrowers are frantically seeking to make arrangements with their lenders, while multifamily borrowers with federally backed mortgages can receive forbearance from Fannie Mae and Freddie Mac as part of the federal stimulus package.

Unfortunately, investors will have to wait for earnings season to reveal just how good or how bad business conditions are within the banking sector. But the Fed’s actions last week suggest the central bank’s leaders do not like what they are seeing. The tempting 4%-8% dividend yields being thrown off by many of the leading mega and regional bank stocks might be best to avoid for the time being.

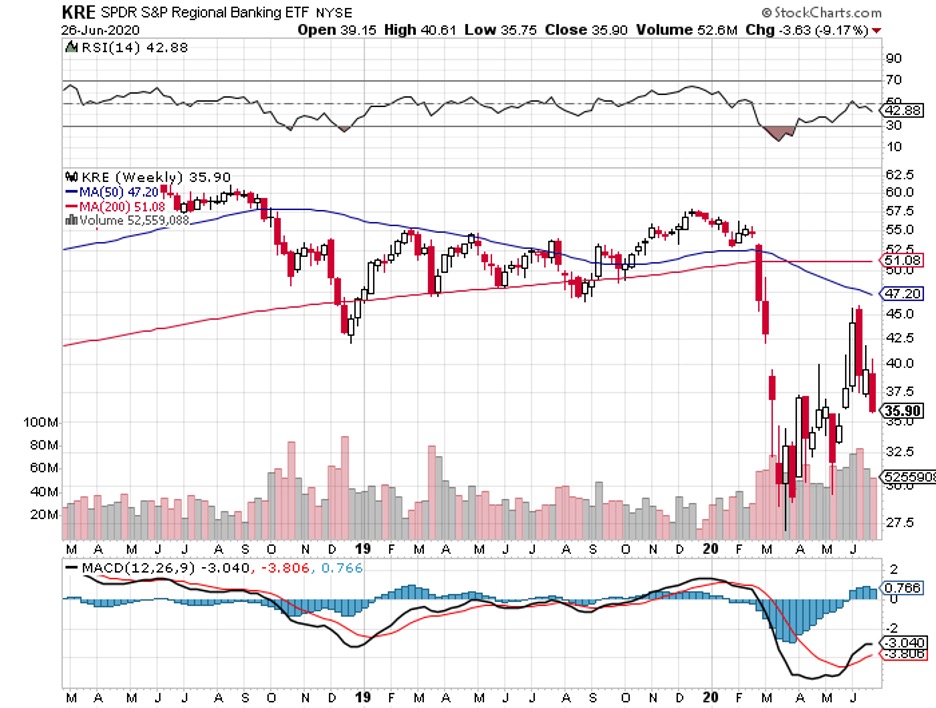

Following a powerful rally from the middle of May through early June, most of the stocks that make up the banking sector have retreated to levels that are just above the March lows, sorely lagging the broader stock market. There are plenty of other places to go in the stock market for dividends yielding 3% to 5% that are “money good” now for the foreseeable future.

Buying bank stocks that are being deeply discounted right in front of earnings season is, in my view, one trade to pass up. If the charts don’t lie, then the chart of the SPDR S&P Regional Banking exchange-traded fund (ETF) (KRE) should raise a red flag for all of those people thinking of initiating or adding to positions in what poses to be a very challenging reporting season.

![[instant messaging via tablets and phones]](https://www.stockinvestor.com/wp-content/uploads/shutterstock_125411345.jpg)