Within the lyrics of the global hit “Wind of Change,” by the German rock band the Scorpions, are the words, “the future’s in the air, I can feel it everywhere.”

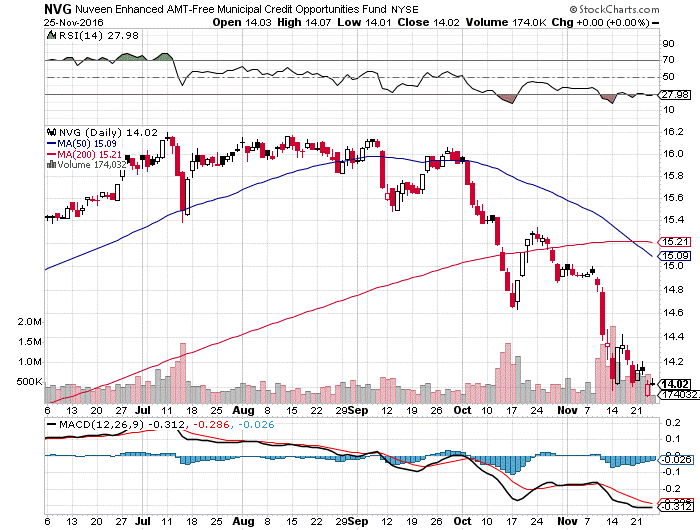

For stock and bond investors, it would be hard to find a better way to pretty much say it all. As the great unwinding of the bond market began in earnest the day after the election, fixed-income investors and holders of what are deemed “equity bond equivalents” — preferred stocks, utilities, most real estate investment trusts (REITs) and consumer staples stocks — have been involved in a slow-motion train wreck. Leveraged closed-end municipal bond funds suffered the steepest losses in valuations. As a case in point, a half-point move up for the 10-year Treasury has inflicted roughly a 13.5% hit on shares of one of Nuveen’s flagship tax-free closed-end bond funds.

Source: Stockcharts.com

So much for the safety of the bond market. Any bonds with maturities out beyond seven years are feeling the pain of constant selling pressure that started in early October as the market began to price in a December rate hike well before the turmoil brought about by the Trump win. His election on Nov. 8 as the next U.S. president simply fueled another leg lower for bonds.

Seeing what lies ahead for income investors requires understanding how so many catalysts have emerged so suddenly. Examples include the fast tracking of a major infrastructure project spending bill with the blessing of soon-to-be Senate Majority Leader Chuck Schumer, the passing of broad cuts in corporate and personal income taxes, a re-working of Obamacare, the de-regulation of certain banking laws and the tax holiday for corporations to repatriate capital held outside the United States. Add in the re-negotiation of major trade deals, and the animal spirits of bullishness are on the rise.

But if these prospective plans, of which none have fully materialized, weren’t enough, the economic calendar has delivered a bevy of solid data points clearly showing an economy already shifting into another gear well before any of Trump’s economic plans kick in. This past week, released data showed better-than-expected reports for Durable Goods, business spending, preliminary Black Friday sales and existing home sales. Anecdotal evidence from my Black Friday trip to Tysons Corner Shopping Mall in McLean, Virginia, at 10:00 am quickly showed by noon that American consumers were not just looking, but instead weighed down by shopping bags. It is going to be a robust Christmas.

Against all this newfound optimism, bond yields have spiked. The 10-year Treasury yield closed the week out at 2.37% and the 30-year Treasury finished at 3.02% with the Dollar Index (DXY) rising to a 14-year high of 101.50. In any other week preceding the election, these two situations would have been viewed as decidedly bearish simply because the prospects for growth have been so low that these headwinds would most certainly be a rally killer. But the winds of change at 1600 Pennsylvania Avenue have market participants turning what some might say is a blind eye to potential headwinds of a breakout dollar and higher interest rates that add stress to borrowing costs. And we’ll know just how stiff these headwinds are when forward corporate guidance is made known in January during the fourth-quarter reporting season.

Until then, income investors trying to stay ahead of the yield curve are rapidly shortening up bond maturities and rotating heavily into dividend-paying cyclical stocks. There has been great consternation by bond and stock investors alike anxiously waiting, almost desperate, for a short-term sell-off to be able to reposition portfolios into shorter-term instruments and up weightings in rate-sensitive dividend stocks. The quandary facing them is that the market has this totally figured out, nary giving an inch but forcing the hand of nervous holders into capitulation mode as the market continues to trade against them in a manner that is eroding capital.

The Rise and Fall of Sentiment and Fear — A Contrarian Pivot Point

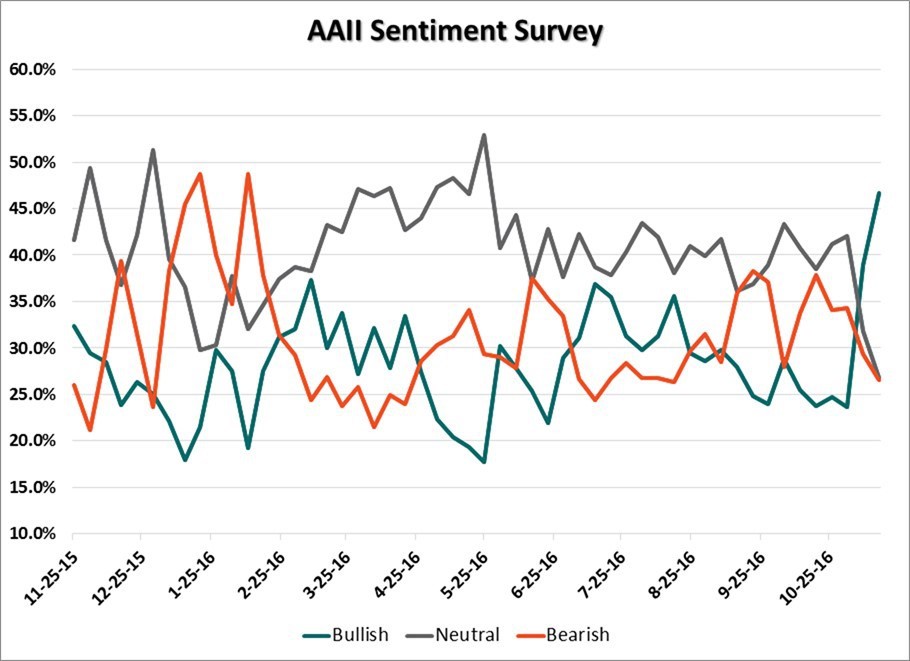

Optimism about the short-term direction of stock prices continues to rise, reaching its highest level in 21 months. At the same time, neutral sentiment fell to a two-year low in the latest AAII Sentiment Survey. Pessimism is also lower. Bullish sentiment, expectations that stock prices will rise over the next six months, jumped 7.8 percentage points to 46.7%. The previous high of optimism, measuring 47.0%, occurred on February 19, 2015. The jump keeps optimism within its typical range, but above its historical average of 38.5%.

Bearish sentiment, which can be defined as expectations that stock prices will fall over the next six months, declined by 2.8 percentage points to 26.6%. The historical average is 30.5%. During the past two weeks, optimism has risen by a cumulative 23.0 percentage points — the 14th largest such move in the 29-year history of the survey. There isn’t a clear trend as to how the market has performed following unusually large two-week increases in bullish sentiment. The median six-month gain for the 13 periods when there was a larger two-week increase in optimism was 5.9%.

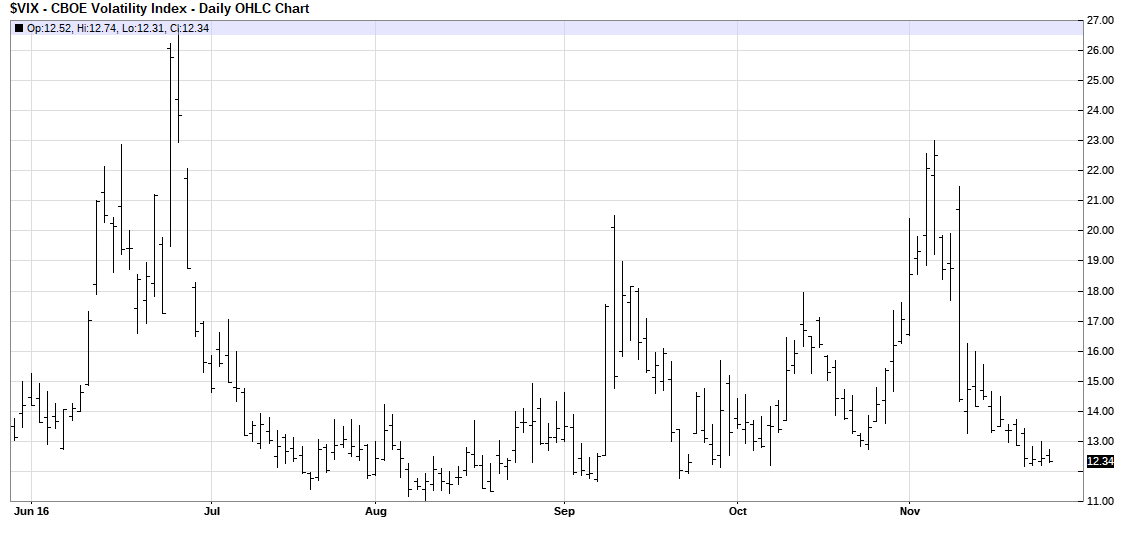

This radical shift in such a short period has all but removed any real evidence of fear about any sort of near-term market risk-off event as the closely watched CBOE Volatility Index (VIX) has tanked to a reading of 12.34 as of Nov. 25. These readings from the charts of both the AAII Survey and the VIX tend to denote short-term peaks and troughs that precede an uptick in market volatility and a downturn for stocks.

My guess is that when the Trump honeymoon fades and the tough reality of making good on all of his campaign promises as they are met with all manner of special interest resistance, some of the bloom will come off the rose-colored rally. Not so significant is that it changes the new trend in place that plays to higher interest rates and a higher rate of U.S. gross domestic product (GDP) growth. Trump won a populist-style election and owes no one any favors. As such, Trump will have greater freedom to build support in both the House and Senate to act favorably on his agenda.

British economist John Maynard Keynes was famously quoted as saying, “the markets can remain irrational longer than you can remain solvent.” And there is a lot of truth to that, especially for those using margin to leverage their bond exposure. We’re in one of those periods that could well frustrate fixed-income investors and holders of defensive stocks right through December as professional fund managers scramble to window-dress portfolios to reduce weightings in these sectors. It’s a massive unwinding of a very crowded trade and just goes to show that when the winds of change are in the air, it pays to turn down the music and get busy making the necessary changes to protect one’s nest egg.

If you want my guidance about how to profit in uncertain times, click here.

In case you missed it, I encourage you to read my e-letter column from last week about the pros and cons of ‘Trump economics.’

“Congratulations on your work. It has been a long slog to get the national accounts…

The broken wing butterfly and the butterfly spread are two different types of option trading…

The bear call spread and the bear put spread are option strategies used when an…

It’s not often that you hear the brilliant Austrian school economist Ludwig von Mises referenced…

While Charles Dickens’s famous statement, “It was the best of times, it was the worst…

Five advantages to day-trading with a 90% win rate offer a tempting opportunity. The five…

{kind=link}

{kind=link}

{kind=link}